You had us at “Subscribe”!

(Image Source: https://www.ayearofboxes.com/)

A lot has been said and researched about millennials. We millennials (yes, I guess I’m voluntarily disclosing my age bracket here), have been called a number of things, mostly not very flattering. Time Magazine has called us “lazy, narcissistic, and entitled”, but in the same article, also calls us “Saviors”. Such constant contradictions are also what make us unique. Our phones are an extension of us, and yet – we’d rather keep a phone conversation one-dimensional, and would much rather just text someone than call them. We love to buy online, but do not want to be “sold” to. We don’t want to commit to a product in an as-is condition, we’d much rather pick and choose what we want.

(Image Source: https://www.theodysseyonline.com/time-stop-hating-millennials)

As a millennial and a marketer myself, I too, am self-contradictory in many ways. I would love to try out new brands and products, but I hate the act of actually setting foot into a store and shopping. So, the idea of having an option to just subscribe to a smorgasbord of products that I would like to try, and have them sent to my doorstep, is very appealing. And I know that I am not an exception – there are many other millennials who are just as mall-averse as I am. And then, there are also many of us that are tempted by the idea of having access to a variety of options to choose from, because what if, heavens forbid, we end up missing out on something?!

There is more to this phenomenon than the emergence of the ‘subscription economy‘, and this is more than an evolution of a business model. This is about the shift in purchasing power to millennials, and a fundamental cultural shift in consumption, driven by the way that this generation buys. Now remember, we are the generation that not only legitimized and achronymized the fear of missing out, but we are also the same generation that is admittedly so narcissistic and often self-serving that we genuinely believe that we deserve the best, and more of the best, and as often as we like.

Which is why, the landscape for brands is now completely altered. While customer loyalty was never a given, it is more of an earned privilege now than it ever was. That said, brand loyalty is not quite dead yet. The real development here, is the emergence of the ‘Curation’ economy – when your shopping basket and your wishlist are essentially like a Pinterest board. We’ve all witnessed the end of the ‘one size fits all’ approach, and watched it evolve into the era of customization. But we have now even moved beyond just plain customization, to the era of handing over the control to consumers, knowing fully well that they may not necessarily want to “commit” exclusively to your brand.

Yes – this commitment-aversion too, is yet another millennial-ism. Unlike our parents, the baby boomers, many of us think that “marriage” in the social context as well as the business context is a nice-to-have, at best. Which is why, we don’t see the need to be “married” to a brand, even if we’re really happy with it. We’re fondly nostalgic about the brands that we grew up with (case in point: AOL Instant Messenger), but the nostalgia has not necessarily translated to active usage/consumption in our adulthood – except, of course, in the case of cult brands like Google, Apple that have maintained their relevance over the years. We want to test everything that’s out there, in the quest of figuring out what works best for us. We want variety, but on our own terms.

Such millennial-isms of ours are being enabled by the ever-increasing plethora of subscription services that provide an assortment of products across categories like beauty, home cooking, personal grooming, fashion, d-i-y crafts, healthy meals, fitness, etc. to name a few. Luxury concept subscription boxes are in a league of their own – with services like ‘Quarterly‘, you can even get assorted subscription boxes curated by your favorite celebrities – so not only are you signing up for the variety, but you are sign up for the unique, curated experience. ‘Try the World‘ lets you try gourmet food from across different countries, every month. All you have to do is choose your assortment, sign up for a delivery frequency of your choice (usually monthly), set up a recurring payment, and then wait for your subscription box to get to your doorstep. And before you start to think that this is getting predictable – there is even a ‘care package’ subscription for women to help with premenstrual blues “to fulfill your cravings, feminine care, and pampering needs that will help you feel better and lift your spirits.” In conclusion, whichever product category you want to try out, chances are – there’s a monthly subscription box for that, just a click away.

We may have already reached the peak of the subscription economy boom. Unsurprisingly enough, a pure curated subscription-driven model alone is not a sustainable model that can be expected to bring profits in the long run. The numbers simply don’t add up in the long run, and economies of scale (especially on eclectic, niche assorted boxes) are an elusive target. So the question that remains is – is the subscription economy a bubble that is about to burst?

The subscription economy does not necessarily have to be a bubble. There is a way for it to achieve its true purpose – which is, to provide millennials the variety that they are seeking and the control that they desire, and still manage to make money from the endeavor – this really is an opportunity for every brand to leverage. In fact, the subscription economy enjoys a very unique advantage in this context – it is only in this unique ecosystem that variety-seeking behavior and brand loyalty can peacefully co-exist (potentially).

Imagine the possibilities if other brands too found a way to engage us attention-deficit-struck millennials via monthly sample-sized subscription boxes that we don’t mind paying a little premium for. Subscription-driven businesses like Birchbox, have found an additional way to keep its audience engaged via brick-and-mortar stores where members can “BYOB” (build your own box). And non-subscription driven business have also begun to catch on. For instance, in a genius move that both squashed competition and added a steady stream of additional revenue, Unilever bought over the blue-eyed baby of the subscription economy – Dollar Shave Club in 2016. Allure magazine offers a monthly “beauty box” containing beauty and makeup items. Starbucks offers two subscription options: One, a subscription service where you can BYOB (as referred above), and pick the coffee, tea & syrup products that you’d like to subscribe to, and the second, to the “Starbucks Reserve Roastery Subscriptions” which are exclusive “micro-roasted” blends that coffee connoisseurs can access. Free-of-cost, self-reported intelligence on customer preferences, and opportunities to cross-sell are among the many other reasons why this is a brilliant move. Amazon has a “Subscribe and Save” option for products that they know are likely not one-time purchases , as well as a “Prime wardrobe” clothing rental/subscription service – which are win-wins for both Amazon and its customers. Customers end up saving money on products if they subscribe, and Amazon gets a steady stream of revenue from these subscribers.

-

(Image Source: http://nypost.com/2013/10/17/rent-the-runway-opens-first-showroom-in-nyc-2/)

My favorite subscription economy success story though – is Rent the Runway (RTR). The fashion startup, often touted as the “Netflix for designer dresses” eventually realized that as fun as subscription boxes are, the steady revenue needs to come from a steady premium source. In May 2016, they launched an ‘unlimited package’ for a $139 a month, letting customers rent three items at a time with unlimited exchanges. The intended audience for this program, was obviously the ‘power users’ of the RTR website – the frequent renters. While this higher price point took a little longer for customers to swallow – it is also now the reason that RTR was able to enjoy profitability (and a $60 million investment from Fidelity) for the first time since its inception in 2009. This program that was originally the ‘bitter pill’, went on to account for more than 20% of RTR’s revenues, a proportion that we can expect to only increase. (Update: Beginning October 16, 2017, RTR has launched a new clothing rental subscription service for everyday clothing items, at a flat rate of $89. Translation: The fashion subscription space just got even more interesting. Let’s wait and watch!)

This is not very different from the good old 80-20 principle logic. This is what keeps airlines afloat – most of their revenues on a full flight come from the first class passengers, not the economy class. Is this not the reason that customer loyalty programs exist – to engage, nurture, and reward your best customers?

These possibilities in no way signal the death of brand loyalty – but rather, they are a sign of the changed times, of how ‘loyalty’ has radically evolved – and how it can in fact, be more profitable and sustainable. Millennials often get a bad rap for being fickle, but the truth is that we are in fact, the most brand loyal generation. In fact, despite the millions of options that we have around us to choose from, we are actually becoming increasingly more loyal (yet another millennial contradiction!) – if the price is right, and if we get to exercise control, and if we actually want to ‘subscribe’ to what your brand offers, and what it stands for.

The jury is still out on whether subscription box services are here to stay as a trend, or they are merely a passing fad. But if these companies think outside the box (pun intended), they may just be able to firmly clinch that much-coveted spot in millennials’ wallets and minds. After all, if a curated, customized and unique experience can be nicely boxed up and sent to a customer’s doorstep at the right price point – now that is an offer a millennial worth his/her salt may not be able to refuse.

Is iOS7 really taking us back to the future?

(Image Source: http://www.Gizmodo.com)

As is the case with most things Apple, last week’s iOS7 launch led to polarizing reactions from the tech world at large – and whether you loved the new operating system to bits or hated its guts, you will likely find it hard to ignore all the ado. Apart from the fact that it was launched by Apple in their widely-followed annual Worldwide Developer Conference week; the key reason behind all the negative / positive hullabaloo is that this is not just any visual revamp – this is an intentional, and paradigm shift in design philosophy made by a company that is synonymous with great design and one that can rightfully be referred to as a pioneer that introduced aesthetics to the world of technology.

I do believe that Apple introduced the concept of design to everybody from the top to the bottom of the value chain in technology. Apple made consumers realize that Hey, a gadget can actually not be clunky and cumbersome and can actually look good – something that had never occurred to us as an option earlier. And most importantly, like the famous Steve Jobs quote goes – Apple taught us that Design wasn’t merely the way a product looked, but it was the way a product worked.

Having said that, I must confess – I am not an iAddict, nor am I anti-Apple. I’m fairly Apple-agnostic and choose to rely on the trio of innovation, user experience and actual value as my yardsticks for assessing new technologies and tech products. As a technophile marketer, I may look at the brand name to marvel / frown at how far the brand has come (or not) in terms of Innovation, and as a consumer, I may look at the brand name as a mark of reliability before actually investing in the product. But I do try to not let the brand name stop me from calling a spade a spade.

Which brings me to my thoughts on iOS7, and Apple’s determined step away from the design philosophy they swore by up until now – Digital Skeuomorphism. Apple’s design strategy was developed with an astute awareness of the nascence of the touch-screen smartphone industry. Apple in its strategic brilliance was aware that with the iPhone, they also had to take upon themselves the task of ensuring audiences got comfortable with all the new icons on the display screen in their hands, and could easily find their way around on their devices without the technology getting in the way (Another quote from Jobs). While a very valid albeit challenging goal to meet at the time – it was what birthed Apple’s strategy to go with digital skeuomorphism; which essentially involved designing icons that were easy to decipher and looked exactly like the real-world, physical objects they were meant to replace. (For instance, the ‘Notes’ App icon looked exactly like a Notepad, and so on.) The skeuomorphed icons added a dash of familiarity to an otherwise alien interface.

And this proved to be a uber-successful choice for Apple then, one that not only made adoption of the iPhone easier for technophiles and technophobes alike, but also introduced a new dimension (and color!) to what had been accepted as a two-dimensional visual landscape. iOS creator Scott Forstall as well as the late Steve Jobs himself were known to be passionate proponents of Skeuomorphism.

But is there a chance Jobs and Forstall went too far in their pet project of visual renderings of real-life objects? Probably yes. After all, there were some designs in the Apple skeuomorphic suite that did stick out like sore thumbs in the Apple scheme of simplicity and elegance; on account of being a little too elaborate and rich (and borderline cheesy!). I mean, just look at the icon for the Game Center – green felt and lacquered wood? Really?!

As a contrast, iOS7 aims to get back to the basics with flat designs and revamped icons. Between iOS6 and 7, the design differences are easily noticeable and the texture differences are definitely stark. The figure below features a great comparison tool, from the desk of Belgium-based design student Niel (Twitter: @pawsupforu), via Time Magazine’s Techland.

![]()

Is iOS7 an earth-shattering development? I’m not sure it is. While I don’t hate the new iOS7 look, the Fisher-Pricey scheme of things stops me from liking it too much. There, I said it. Heck, my two-year old nephew has a toy phone that could pass off as the inspiration behind iOS7 – not kidding. The bright, fuschiously vibrant color scheme has sparked off many an internet meme, the most entertaining one being this one. That said, I’m not a designer, so I don’t want to sound like I’m biting off more than I can chew – but here’s a professional opinion specifically on the design elements of iOS7. Yes, design is a subjective thing and everyone is entitled to their own opinions; but if you go strictly by Steve Job’s own definition of it (see Para 2 above) – iOS7 leaves a lot to be desired.

Sure, it has cool interface improvements like a parallax view of the home screen (which lets a background image move around slightly while icons remain in place above it), swooshing transition animations, intuitive lock screens and transparent overlays. But unfortunately (for Apple) – there are other phones that have been doing that stuff (and more) for a while now. So does that mean that WWDCs are henceforth going to be only about tactics to level the playing field disrupted by some other player? Since when did Apple stop being the disrupter themselves?

Before I come across as a certified iRanter, let me state the key thing I want from the next iOS, in advance: All I want from the next iOS is more control. Maybe I’d like a search widget on my phone home screen. Maybe, a real-time RSS feed from Twitter. Maybe I’d like to change the static dock to feature the apps I actually access more often. Maybe I’d like the ability to choose my own default browser. Or maybe, I’d really like using a Swype keyboard on my phone (allowing me to swype through the keyboard as opposed to punching one key at a time). I’d like to at least have the option to make those tweaks, whether I exercise it or not. It is MY phone after all. I want it to “think different”, and be more of me, than of Apple. Too tall an order? Shouldn’t be so, right?

I’ve loved my iDevices for the sleek hardware and reliable software – I still sorta do. But from a competitive strategy perspective, both those competencies are now the stuff that is anyway expected of any smart device worth its salt. They’re necessary for succeeding in the market, but not sufficient anymore. Agreed, it was very much an Apple core competency to get the magical hardware + software combination right, but other players have started getting it right too.

Proponents of iOS7 and hardcore iFans have welcomed the end of skeuomorphism by saying it was redundant as it was the solution to a problem that Apple no longer has. While that may be true (and while I’m aware iOS7 is not just about skeuomorphism and also aims at providing a new user experience), I do tend to believe that the irony of iOS7 in turn is dual: A. It fails to address the problem(/s?) Apple actually has; and B. The bottle may have changed and become prettier (debatable adjective, perhaps!) – but the wine is sadly more or less the same.

Is the Internet of Things the future of narcissism?

Great food for thought, extends the Validation vs. Vanity debate to the ‘Internet of Things’. The writing’s on the wall, or rather, throughout our digital footprint across devices, and across the worldwide web!

This post is pure genius! Absolute must-read.

Access to rich usage data is something that is a defining element of modern product development. From cars, to services, to communications the presence of data showing how, why, when products are used is informing how products are built and evolve. To those developing products, data is an essential ingredient to the process. But sometimes, choices made that are informed by data cause a bit of an uproar when there isn’t uniform agreement.

Access to rich usage data is something that is a defining element of modern product development. From cars, to services, to communications the presence of data showing how, why, when products are used is informing how products are built and evolve. To those developing products, data is an essential ingredient to the process. But sometimes, choices made that are informed by data cause a bit of an uproar when there isn’t uniform agreement.

The front page of the Financial Times juxtaposed two data-driven stories that show just how tricky the role of data can be. For Veronica Mars fans (myself included), this past week was an incredible success as a Kickstarter project raised millions to fund a full length movie. Talk about data speaking loud and clear.

This same week Google announced the end of life of Google Reader, and as you can see from the headline there was some…

View original post 1,420 more words

Messengers of Confusion

We all get why marketers choose ambassadors and evangelists for their brands. They help put a face and name to the brand, and add a human element to the perceived experience of using the product that the brand advocates. They also personify the sky-high stack of values that marketers hope their audiences associate with their brands, and strike that elusive chord of emotional connect with those audiences. Long story short, ambassadors and evangelists are intended to be catalysts in the Attention-Interest-Desire-Action-Recommendation cycle. And the choice of brand ambassador is supposed to make their audiences go: “Of course, that makes sense.” and NOT “Err.. What were they thinking?!”

Lately, though, there is an increasing number of brands whose choice of ambassadors seems to be more a cry of desperation, than a positive reinforcement. Don’t get me wrong, the chosen ones in question are super successful and admired people in their field. By themselves, their own personal brands are associated with all things positive. But it’s their association with certain brands that comes across as completely random, and honestly, just plain sad.

(Image credits: jessicaalbalove.tumblr.com)

Take the Windows Phone, for instance. Jessica Alba is the face of the phone, and in all their commercials, press conferences, and other public interactions – the key reason that is claimed as the basis of this mutual association (Alba’s home & baby products venture ‘The Honest Company’ shares space in Windows phone promotional material), is that the Windows Phone works for people like Ms. Alba who have to multitask and juggle between diverse parts of their lives efficiently. Frankly, the whole premise of this association is weak-sauce, and it’s presented in a way that’s not really helping Microsoft’s case. Sure, the phone has clever features like the ‘Kids’ Zone’ that makes sure your kids don’t get access to any of your stuff on your phone (and thereby, don’t get to delete / tinker Apps around on your phone!). I also quite like the ‘Live tiles’ interface – interesting stuff, very Flipboard-esque. But I still don’t see any clear proposition and distinct advantage that makes me want to switch over to that phone. Also, no offence to Jessica Alba, but they may as well have used anyy other seemingly multi-tasking, well-liked celebrity as their endorser and I bet nobody would’ve wondered: “Hey, I wonder why they didn’t choose Jessica Alba as a brand ambassador!” It’s not a no-brainer association. Or even something that instantly clicks.

(Image source: http://www.engadget.com)

Another such “association” that is hard to comprehend, is the Alicia Keys – Blackberry 10 alliance. As if featuring her as a brand ambassador wasn’t confusing enough, Keys was appointed as ‘Global Creative Director’ for Blackberry (I’d love to see the job description for this one!). I know the Querty ‘Keys’ have always been one of BB’s trump cards, but isn’t this taking it a little too far?! Also, it’s not like Blackberry wants to leave their established positioning as a business phone behind: With the BB 10, they basically want to be a business phone & more for “people who want to get things done”. Apart from the obvious vagueness of that statement, it implies that BB now wants to be everything for everyone: a classic recipe for marketing disaster. And as much as I love Alicia Keys, it’s hard to digest her pantsuit-clad, Blackberry-brandishing Avatar: It’s just doesn’t make for a convincing story; and incidents like her continuing to use her iPhone to tweet (and later attributing it to hacking) are not helping the case either. Let’s just say this girl isn’t exactly on fire here.

(Image credits: http://en.inmoreau.com)

The Justin Timberlake – MySpace alliance is one more such confusing story. But it may be worth watching this one closely, as there are two different factors in the mix: 1. Timberlake himself is the unlikely entrepreneur here and has invested $35 million in MySpace and released a new single exclusively via the platform, and 2. MySpace seems to be poised for a huge overhaul in terms of its design (getting rid of the clutter), quality of content, and focus: Timberlake plans to leverage the “social component to entertainment” by bringing fans and artists together in a more organized community on MySpace. So, the jury may still be out on this one.

To me, an example of a ‘no-brainer’ choice for brand ambassadorship would be Tiger Woods for Nike. Yes – despite all the scandals of the past couple of years, I think Tiger Woods still is a good choice for Nike – as opposed to Lance Armstrong, who has obviously earned his dismemberment. Reason being, while the personal character of Tiger Woods may be questionable, his professional capabilities and achievements cannot be doubted. On the other hand, with Lance Armstrong – the very reason for his glory: his performance on the cycling track – can no longer be held as the golden standard. And Nike is, after all, about performance. Nike never said it represents good husbands, or good family men – it only said it represented go-getting, performance-oriented stellar athletes and sportspersons. And his personal life notwithstanding, Tiger Woods still personifies this performance-driven perfection that Nike is all about.

There are plenty such great brand ambassadorships around. Take the case of Jennifer Hudson‘s much publicized, winning battle against the bulge courtesy Weightwatchers, for instance. Or the long standing James Bond – Omega association. Or heck, even John Stamos and Oikos – what better way to underscore the Greek-ness (and ahem, appeal) of their brand?! These ambassadorships make sense, not just because they make people sit up and notice the brand, but more so because they echo the exact qualities that the brand clearly wants to highlight, and they speak directly to the purchase decision maker. While it is true that the right ambassador could work wonders for a brand, it’s not an imperative to success. And whether or not marketers choose to enlist celebrity ambassadors – it’s high time they reminded themselves that their brand is supposed to be the hero of the story, and the ambassadors merely the narrators and messengers of it. Not the other way around.

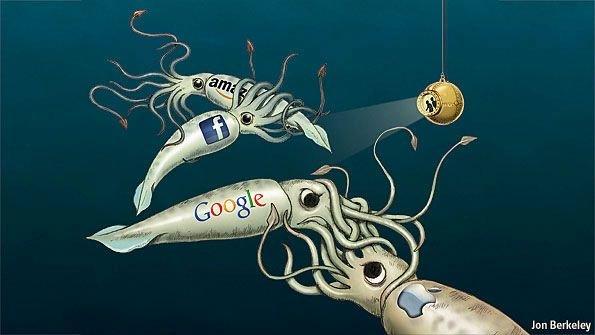

Clash of the titans

(Image source: iqballatif.newsvine.com)

The world of management consulting has its Big 4 – the accounting/professional services firms KPMG, Ernst & Young, Deloitte and PriceWaterhouse Coopers, the Goliaths that define the industry and make competitors in that space inconsequential and insignificant. Which is why it seems like quite a coincidence that the increasingly convergent world of technology and business too is dominated by four Goliaths: Amazon, Apple, Google and Facebook.

But is it really mere happenstance that the Big 4 of the business/technology world are just who they are? Probably not.

Over the years, the Big 4 have evolved from being simple product/service providers to comprehensive, repurposable platforms that shrewdly collate the required competencies of any online business:

- Data: Intelligence on Consumer Demographics, Actions/Behavior, preferences

- Devices: Desktop, Mobile, Tablet, and the Cloud

- Distribution: Collate, distribute and publish unique content

- Sociability:Sharability and conversation-worthiness

- Findability:Of accurate as well as geographically relevant information

The inherent similarity between the Big 4 is that they each are more an assortment of inter-related services (= Benefits and Values) than a singular product (= Feature). There is, of course, scope for improvement for each on these turfs and it’s not quite a level playing field across all product categories yet – a fact which they each are well aware of. Even so, as the Big 4 work on gaining competencies in new turfs and dialing up the aspects that they are not-so-competent in yet, the lines between categories, industries and software/hardware have increasingly started to blur. Here’s a strategic overview of how the Big 4 have been slowly yet steadily making forays into each other’s turfs.

AMAZON:

Last Quarterly Revenue: $13.8 bn | Last Quarterly Profit/Loss: -$274 mn | Market cap: $117.1 bn | Gross margin: 25.3% *

(Image source: http://www.teleread.com)

Amazon’s core competencies lie in E-Commerce, Distribution and Publishing. They have made a successful foray into the Device side of the platform via Kindle, and are rumored to be working on an Amazon phone that will be based on an Amazon-exclusive version of Android (“Amdroid”).The phone, like other Amazon extensions / diversifications will be aimed at ensuring you buy more from Amazon; and also provide Amazon more intelligence on your buying behavior and preferences – thereby supporting their core business.

What next? Amazon needs to become more responsive to competition. Until recently, Amazon played the role of Challenger well in the tablet market. But after Apple’s punch-packed response in the form of iPad Mini, the once-clearly defined boundaries between the target audiences of Apple’s iPad and Amazon’s Kindle have now blurred. Amazon will need to define the Kindle’s differential value (if any) better, and given that Amazon has been selling Kindle at a loss, either the price-point or the offering itself needs revision. There can be no doubt that Amazon has a bright future ahead, and the sheer length and breadth of its portfolio is astounding. Amazon is a shining beacon of service-orientation; where service-orientation is actually the common denominator across the architecture, culture and operations of the company. Another unique aspect about Amazon is its symbiotic relationship with a co-member of the Big 4 – Google. However, the extent of their dependence on Android (and thereby, Google), is potentially also a huge risk in the cut-throat context of the Big 4.

APPLE:

Last Quarterly Revenue: $36 bn | Last Quarterly Profit/Loss: $8.2 bn | Market cap: $489.3 bn | Gross margin: 40.2% *

2013 could prove to be a landmark year for Apple. As the most valuable company in the world, it has successfully made its presence felt across a good part of the tech ecosytem, ranging from hardware to software to distribution; Apple has yet to make a satisfactory mark for itself in the Search, Social and Data domains. To say their move to keep Google out of the geographical search domain out of the iOS sandbox has failed would be an understatement to an extent. Not only was Apple forced to bring Google maps back on iOS, they were also forced to come to terms with the reality that when it comes to anything Search (and Data collation related), Google is still very much the leader and Apple cannot claim to be a worthy challenger yet. Nonetheless, the reason 2013 could just be the year that features yet another genius innovation from Apple, is because Apple is working on converging Social , Data and Distribution together in a feature-loaded ‘iTV’, a move that tantamounts to bringing Apple, Facebook and Amazon together in your living room.

What next? If there’s a company that actually has the financial bandwidth to build a platform of interlinked products in the immediate future, it’s Apple. Apple gets platforms and has a great grip on consumer insights (well, at least so far). Apple is great at rocking the boat, and challenging the status quo, and improvising on the existing. However, Apple does not get the concept of ‘Openness’, be it Open access or Open source. The time to re-evaluate the boundaries of the ‘sandbox’ may be closer than Apple would like to admit. Also, times have changed, and the need of the hour is for Apple to play defense (ideally, in the market and not the courtroom!) all the while not losing steam on innovation.

FACEBOOK:

Last Quarterly Revenue: $1.26 bn | Last Quarterly Profit/Loss: -$59 mn | Market cap: $58.3 bn | Gross margin: 74.5% *

While Facebook is the leader in the sociability aspect of the game, findability is definitely a work-in-progress area for them. They’ve tried to upgrade their Search functionality in the summer of 2012, a move which has brought them a few steps closer to becoming a Social Search engine. Mark Zuckerberg offered a very matter-of-fact summary of the move: “Facebook is pretty uniquely positioned to answer the questions people have’ – and plans to build more powerful search facilities as Facebook evolves.” Key phrase to note obviously being, “uniquely positioned to answer the questions people have“. And in spite of the sheer goldmine of data that Facebook has at its disposal (Of course it does, who are we kidding!) – they have miles to go in actually leveraging that data effectively, beyond its already launched Facebook Ad Exchange and Facebook Ads targeted/retargeted advertising solutions.

What next? Facebook has access to the most-envied goldmine of consumer intelligence, and yet has always seemed to be indecisive and noncommittal about what it intends to do with it. Part of it is attributable to the fear of public backlash against using that data, but most of it has actually been because of the lack of clear vision on the the matter. They seem to be in constant experimental mode here, and that may prove to be detrimental to their cause.

GOOGLE:

Last Quarterly Revenue: $14.0 bn | Last Quarterly Profit/Loss: $2.2 bn | Market cap: $233.1 bn | Gross margin: 53.7% *

A key fact to keep in mind when we evaluate Google, is that as far as search goes – it is still a Google world. Per a December 2012 comScore report, Google owns about 67% market share, while the second-in-line Bing trails at a distant 16.2%. The

Android vs iOS

other trump card Google has in its repertoire is Android. The International Data Corporation (IDC) reported that 3 out of every 4 smartphones shipped out in the third quarter of 2012 were Android-based. Meanwhile, Google Plus, as we know is Google’s not-so-successful attempt at conquering the world of social networking. While the API-starved network may have well become Google’s very own ghost-town, there’s reason to believe that Google Plus could evolve into the product that is the face of the Google platform – given how Google has begun unleashing its Search horsepower and content ranking capabilities on Google Plus, along with the integration of other unique features like hangouts, circles and other weapons from Google’s holisitic arsenal.

What next? Google has its groundwork in place as far comprehensive platforms go. They have been shrewd enough to preempt the universal applicability of their main source of livelihood: Search (and Data-based intelligence). And they have been clever in initiating the open source/ Android movement years ago to restore balance in the i-Dominated smartphone world. They need to, however, ramp up their competencies in distribution/publishing and also social. Most importantly, they need to invest resources in developing well-rounded products that are actually good-to-go, as opposed to launching knee-jerk reactionary products (case in point: Google Plus) and then developing them on-the-go. Google needs to now prove that as far integration goes, they’ve still got it.

Now here’s a quick infographic to gauge how the respective platforms of the Big 4 stack up against each other.

The argument about who is destined to win this clash will probably continue for a while. But it is clear that the player that will emerge a true winner from this clash will not be the one that launches the most innovative product of the decade, but the one that manages to integrate all its products into a single, tightly knit ecosystem that creates perceptible value for the consumer. Each of the Big 4 likely stands an equal chance of being able to crack this code – or maybe not. In any case, there are exciting times ahead for sure – for technology, innovation and business in general. And whoever the winner proves to be, my hope is that in the end, it is we the consumers who gain the most from this epic clash of the titans.

* Key financials sourced from The Wall Street Journal

The Secret Caveat of Brand Karma

What goes around…

(Image source: rotflpictures.com)

We’ve all heard those quotes reminding us how the true test of one’s character is during hard times. Last week reminded me of how true this holds even in the case of inanimate Brands. Up until now, I genuinely believed this is common knowledge, and something every brand, every marketing team, and every social media community manager is aware of.

American Apparel’s ‘Hurricane Sandy Sale’ Email

Turns out, it isn’t. On October 29, while Hurricane Sandy was in devastating full swing and in the middle of its terrible rampage across nine states along the east coast, American Apparel sent out an email (included on the right) specifically targeted to consumers belonging to these nine states, inviting them to shop online in case they were ‘bored’ during the storm. No concerns about the well-being of their consumers mentioned, no help offered. Needless to say, Twittersphere exploded with criticism for AA, and this insensitive faux pas has brought some seriously bad PR to AA shores.

But does AA care? Nah. Their CEO Dov Charney said on record that this wasn’t really a big deal, and he doesn’t think his marketing team made a blooper. His exact words were: “Part of what you want to do in these events is keep the wheels of commerce going.”

While I do appreciate Mr. Charney’s commitment to constantly keeping an eye on the ball, he unfortunately doesn’t seem to acknowledge the fact that the “wheels of commerce” are the last thing on people’s minds when they’re going through a life-threatening natural calamity. And a result, a brand which blatantly admits it’s only thinking about keeping the cash registers ringing through rain, storm and disaster will obviously ruffle many feathers.

Gap checks-in to “Frankenstorm Apocalypse – Hurricane Sandy”

Another kindred brand that attempted to make light of the situation is Gap. They decided to ‘check-in’ via Foursquare on a “Great Outdoors” category spot they’d specially created: “Frankenstorm Apocalypse – Hurricane Sandy” (See image alongside)

Incidents like the above make American Apparel and Gap look like “bad person” brands who don’t really respect the feelings of their audience. And that may not bode very well for them, especially given how powerful negative word of mouth can be. In fact, according to a recent Retail industry roundup by About.com, a whopping 140 million people on Twitter found American Apparel’s Sandy Sale offensive and inappropriate. While we don’t have a way yet to directly translate this number into impact on sales, we can take it as a good indicator of purchase intent at the very least – which of course is by no means a number American Apparel could afford to risk. And Gap faced the music as well – featured below is just one among the several irate responses they received.

Reactions to Gap on Twitter

In contrast, Starbucks has been surprisingly humane and empathetic pre and post Sandy. Yes, I say ‘surprisingly’ because of the reputation Starbucks earned for themselves following their indifferent treatment of the 9/11 rescue workers in NYC back in 2001. But that was then, this is now. Not only did Starbucks announce they were shutting their stores early for the safety of their employees, but they also made sure their consumers knew they were being thought of, and their well-being was being hoped for, via their various social media channels. They also made sure consumers were kept posted on what Starbucks’ response was to the hurricane. In addition, post the storm, they also urged their audiences to make a contribution to Red Cross to help rebuild the areas affected by Sandy. How much of a tangible difference does all this really make to the lives of people actually affected by the storm? Maybe none. But it sure has made people think of Starbucks as every bit of the warm, community brand they claim to be, in stark contrast to the unapologetic indifference of brands like American Apparel.

What’s even more impressive is brands like Verizon that are choosing to actually put their money where their mouth is. Verizon just announced that they’re going to waive domestic voice and text charges for customers in the areas affected by Sandy. That’s an even bigger step than AT&T and Sprint who announced they would waive off late charges for hurricane victims who were not able to pay off their phone bills on time because of the storm. (Sure, if Verizon had waived off even Data charges – they would be considered the Angels of Telecom-land, but waiving the voice-text charges too is a pretty substantial step in itself!)

Be it Verizon or American Apparel, there are several such instances of brands showing their compassionate side or self-serving side in the face of hurricane Sandy. By choosing to reach out to consumers during the storm, these brands could only meet one of two consequences: 1. Be lauded for their sense of customer service and gain more emotional capital; or 2. Earn people’s wrath by attempting to capitalize on a tragic situation or being unabashedly indifferent to it. In either case, thanks to social media, the side-effect is always amplification. Good deeds and bad deeds alike are amplified, shared virally and by the time a brand can react to it – acquire the status of a socio-urban legend. For instance, Radian 6 recently reported that Hurricane Sandy triggered 11.5 Million social media conversations. Imagine the kind of wanted / unwanted amplification a brand would stand to gain against this backdrop.

It’s not just the sheer money-mindedness behind the sentiment displayed by American Apparel and Gap that is so controversial. What these brands seem to have completely missed is the fact that in the age of social media, for all practical purposes; they are viewed as a real person with a voice and personality by their audiences. The KIND of person they come across as, however, is their choice. And this is exactly why brands need to have good karma. Because at the end of the day, whether it’s Starbucks checking in on their customers’ well-being or P&G dispatching Duracell charging stations and Tide laundry trucks for free assistance to hurricane victims, or Verizon waiving off charges for hurricane-hit customers, it does boil down to Karma: What goes around will come around (with amplified effect), especially in today’s socially charged digital times. And by default, it might just be time to institute and operate by a new motto of commerce – Caveat Marketer (Marketer, beware!).

Klout: Validation or Vanity?

(Image Source: http://forfreeblog.blogspot.com)

The surge of Social Media has led to an oft-joked-about side-effect. In addition to aggravating Nomophobia (the fear of being without one’s cellphone) and a general fear of being disconnected, Social Media has led to a rise in an unhealthy obsession with seeking validation. Sure, in theory, it’s great to have constructive feedback and it’s great to know your opinions matter, and that you do influence people around you. But aren’t we taking ourselves a little too seriously when we decide to keep measuring how much “influence” we have, just so our need for attention and self-importance is fulfilled? This is my primary pet peeve about Klout, and the narcissistic ‘Klout score’ metric.

I do get the relevance of such a metric and the need to measure social media influence for Brands and people whose livelihood depends on promoting themselves on social media. And I have to admit, as a marketer, Klout did pique my curiosity and I set about exploring its in’s and out’s with a lot of gusto. But I was quite disappointed when I realized there wasn’t too much science (or logic!) behind the metric, and that Klout can’t really be classified as a legit Validation metric. It’s really only a Vanity metric and an inaccurate one at that.

Klout has always relied on hazy parameters to measure influence, and their definition of Influence is, well, debatable, to say the least. They have a profound-ish explanation of what they mean by Influence on the site, and this little graphic below they’ve featured there is supposed to cover what Influence entails.

Klout “Influence” components

(Image source: http://klout.com/#/corp/what_is_klout)

As is obvious, this implied scope is completely partial to Twitter as Followers, Retweets etc are relevant to only Twitter. Question is, what happens then, to the content we share on other social media platforms? Shouldn’t there ideally be a way to take into account influence and interactions across all social platforms (including Pinterest) accurately? Also, going back to the image alongside, how do ‘Lists’ play a role in one’s Social Media Influence?? ‘Lists’ are just a convenient way for Twitter users to sort their feed. If I have 1,000 Lists on Twitter, how does it indicate my social influence? If anything, it indicates a degree of OCD in me, but I fail to see how having more Lists makes me more influential. Am I missing something here? If anyone knows of an actual relevance of ‘Lists’ to one’s Klout score, please feel free to leave a comment! (UPDATE: Vielen Dank to my fellow-blogger ladyfromhamburg for sharing some great information on this: The ‘Lists’ component of Klout’s definition of Influence shows the number of Lists one is a part of on Twitter. That sure makes more sense, and puts my Lists-related confusion to rest! Now if only Klout would take some inspiration and start decoding all these parameters and more on their site. :))

(Image source: http://www.colleendilen.com)

What further blurs the already fuzzy scheme of things, is the relative weightages assigned to the parameters used to define ‘Influence’. Shouldn’t Klout be a little more transparent about this, especially since it claims to be the “Standard of Influence” that is supposedly meant to empower people who share content online? Does the Klout score include sharing and amplification of content only? Then what is the relative importance of those respectively? For instance, basis what I noticed on my own Klout dashboard – Retweets and Replies seem to have a higher weightage than Mentions. Let me attempt decoding what that effectively means: Only if what you’re saying is being passed on, do you have influence. Okay, this could be partly true – but what about the other part of it where you also need to be listened to, to consider yourself as having some influence? What about all the new followers/subscribers/visits you add with every new piece of content you share? And what about the followers/subscribers you have retained over a period of time? Those people have chosen to stay connected with you as they see some value in it, and find your content interesting. Shouldn’t that account for something?

(Image source: http://www.theanimatedwoman.com)

And what about all the metrics that tell you how many people actually click on the links you share to read your content? Shouldn’t those influence your Klout score as well? As an apparent disclaimer, Klout says in its FAQs: “The Klout score is a reflection of Influence, not activity.” Err, this doesn’t help their case, does it?

Nevertheless, all the anti-Klout sentiment aside – there are a couple of things about Klout that I do find pretty interesting. First, their Brand Squad feature. This basically helps brands identify their influencers and evangelists. This has SO much potential; and if they are able to throw in Sentiment Analysis and Blog-searching capabilities in here, this could potentially be a great one-stop shop social media measurement tool for Brands – one that Klout can actually hope to make some revenues off of.

The second feature that shows promise is – the Perks tool. Of course, in its current form and with its current targeting algorithm (or maybe the lack thereof), it’s fairly useless. But think about the tremendous potential Klout’s ‘Perks’ has: It could serve as Klouts’s very own advertising model to serve targeted offers based on content, influencers and influential topics; as well as retargeted promotions/offers from Brands.

Even so, all the potential genius behind these tools notwithstanding, the fact that remains is – Klout still has a long way to go. Sure, a handful of Social Media mavens may already be judging us on the basis of our Klout score, but it’s going to take Klout a lot many enhancements before it can be taken seriously as an accurate social media metric and a reliable measure of actual social CLOUT, or it won’t be soon before long that Klout has to bow out! (Just couldn’t resist that cheesy rhyme!)

We wouldn’t shop where we socialize. Or would we?

(Image source: http://www.technologyreview.com)

You’ve heard it before, and chances are; you’ve said it yourself: “Why don’t they just stop running all those ads on Facebook?- nobody clicks on them anyway.” You are, of course well-justified in asking this question, since you for one, have never clicked on Ads on Facebook yourself, right? And you also don’t know anyone who clicks on them; either since those Ads are really not relevant, or purely because they’re just an annoying disturbance. So, the big question that remains is: Why DO they advertise on Facebook despite all the apparent ineffectiveness? Why do they still believe there is merit in allocating Advertising dollars to Social Media in general and Facebook in particular?

The fact most of us are in agreement about is, social media works at several levels. It works because it brings together Paid, Owned, Earned and Shared media all under roof. It works because at its very core; it’s a contemporary form of two of the most ancient forms of marketing: Word-of-mouth publicity and Two-way conversation. It works because at the end of the day, all businesses consist of people working with other people – and Social Media helps make your business more appealing to those other people by adding a voice and human quality to your business and brand.

Now comes the debatable aspect of the story. Does Paid-for Social Media marketing give you bang for your buck? Well, if you choose to focus on the right parameters, and remind yourself that this is just the tip of a huge, uncharted iceberg – the amazing potential Facebook holds as a marketing platform shines through all the cynicism.

TBG Digital’s Quarterly Facebook Advertising report (Q1 – 2012) has brought to attention how the engagement rates of Ads on Facebook have dropped by 8% since the end of last year, while Impressions (CPMs) and Clicks (CPCs) have become more expensive for Marketers and have risen by 41% and 23% respectively. However, it’s not that startling a development when you consider the fact that the number of Ads per page on Facebook have increased from 4 to 7. Banner Blindness is a well-acknowledged, universally present online phenomenon – not exclusive to Facebook. Facebook’s problem has more to do with Contextual relevance and Ad placement than mere Banner blindness. As a testimony to that, the same report also brings forth the remarkable success news partners have had on Facebook (Aka the Social Readers) – Click-through Rates for them have increased by a whopping 196% during a three-month period.

In effect, this is what all these statistics point to:

1. Contextual relevance: Don’t show me Ads that are not relevant to me.

An example of a Retargeted Ad via Facebook Exchange

(Image Source: http://www.techcrunch.com)

Retargeted Ads are based on Search and buying history that is recorded via cookies. There is an inherent similarity Facebook shares with Yahoo Mail w.r.t to the way its users interact with the site: Users usually stay logged onto the site on another tab/window while they continue with their other online activities. Key opportunities?: Cookies, and more cookies and therefore a golden opportunity to use Ad inventory for showing Ads that are relevant what the user’s actually been looking for! This strategy has served Yahoo very well, as it most likely will Facebook.

2. Placement: If you show me an Ad where I expect to see it, chances are I won’t click on it (or even notice it, for that matter).

The tremendous success rate of Facebook’s News partners proves that there may be a better way to make users sit up and take notice. Smart, non-intrusive integration of content in users’ news feeds would generate more interest and serve as an Ad in itself. If people see interesting content suggestions in their News Feed they’d actually appreciate checking out basis what they know they have enjoyed in the past; they likely wouldn’t dismiss those off as instantly as the Ads they are inclined to. Assuming of course, they don’t foresee clicking on them to be a cause of potential social embarrassment. 🙂

Which brings us to answering the question brought up at the beginning of this post. The reason marketers still continue to believe it makes sense and cents to include Facebook in their media plans is that Facebook has not only understood the challenges of contextual relevance and Ad placement – but has also taken 3 very promising measures to address them:

A. The Open Graph – which lets users share select activities on Facebook and presents marketers with branding opportunities at those milestones

B. The Facebook Ad Exchange – which makes Facebook’s Ad inventory available to real-time bidding (RTB) and retargeting

C. The ‘Want’ Button – which lets users create their own product wishlists on Facebook

Imagine the plethora of opportunities with being able to target people not just on the basis of WHO they are and WHERE they are, but on the basis of WHAT they DO on a daily basis, and WHAT they WANT. Pure marketing gold.

There is a catch to this, of course. All these functionalities are in varying degrees of nascency currently and Facebook has arrived pretty late to the Retargeting/ Ad optimization party. So whether or not Facebook succeeds in leveraging its true potential and optimizing its revenue stream – is something we will know in due time. If Facebook does drop the ball though, it will be quite a shame, since it is their battle to lose.

(Image source: http://www.marketing.yell.com)

{kind=link}