Blog Archives

Is iOS7 really taking us back to the future?

(Image Source: http://www.Gizmodo.com)

As is the case with most things Apple, last week’s iOS7 launch led to polarizing reactions from the tech world at large – and whether you loved the new operating system to bits or hated its guts, you will likely find it hard to ignore all the ado. Apart from the fact that it was launched by Apple in their widely-followed annual Worldwide Developer Conference week; the key reason behind all the negative / positive hullabaloo is that this is not just any visual revamp – this is an intentional, and paradigm shift in design philosophy made by a company that is synonymous with great design and one that can rightfully be referred to as a pioneer that introduced aesthetics to the world of technology.

I do believe that Apple introduced the concept of design to everybody from the top to the bottom of the value chain in technology. Apple made consumers realize that Hey, a gadget can actually not be clunky and cumbersome and can actually look good – something that had never occurred to us as an option earlier. And most importantly, like the famous Steve Jobs quote goes – Apple taught us that Design wasn’t merely the way a product looked, but it was the way a product worked.

Having said that, I must confess – I am not an iAddict, nor am I anti-Apple. I’m fairly Apple-agnostic and choose to rely on the trio of innovation, user experience and actual value as my yardsticks for assessing new technologies and tech products. As a technophile marketer, I may look at the brand name to marvel / frown at how far the brand has come (or not) in terms of Innovation, and as a consumer, I may look at the brand name as a mark of reliability before actually investing in the product. But I do try to not let the brand name stop me from calling a spade a spade.

Which brings me to my thoughts on iOS7, and Apple’s determined step away from the design philosophy they swore by up until now – Digital Skeuomorphism. Apple’s design strategy was developed with an astute awareness of the nascence of the touch-screen smartphone industry. Apple in its strategic brilliance was aware that with the iPhone, they also had to take upon themselves the task of ensuring audiences got comfortable with all the new icons on the display screen in their hands, and could easily find their way around on their devices without the technology getting in the way (Another quote from Jobs). While a very valid albeit challenging goal to meet at the time – it was what birthed Apple’s strategy to go with digital skeuomorphism; which essentially involved designing icons that were easy to decipher and looked exactly like the real-world, physical objects they were meant to replace. (For instance, the ‘Notes’ App icon looked exactly like a Notepad, and so on.) The skeuomorphed icons added a dash of familiarity to an otherwise alien interface.

And this proved to be a uber-successful choice for Apple then, one that not only made adoption of the iPhone easier for technophiles and technophobes alike, but also introduced a new dimension (and color!) to what had been accepted as a two-dimensional visual landscape. iOS creator Scott Forstall as well as the late Steve Jobs himself were known to be passionate proponents of Skeuomorphism.

But is there a chance Jobs and Forstall went too far in their pet project of visual renderings of real-life objects? Probably yes. After all, there were some designs in the Apple skeuomorphic suite that did stick out like sore thumbs in the Apple scheme of simplicity and elegance; on account of being a little too elaborate and rich (and borderline cheesy!). I mean, just look at the icon for the Game Center – green felt and lacquered wood? Really?!

As a contrast, iOS7 aims to get back to the basics with flat designs and revamped icons. Between iOS6 and 7, the design differences are easily noticeable and the texture differences are definitely stark. The figure below features a great comparison tool, from the desk of Belgium-based design student Niel (Twitter: @pawsupforu), via Time Magazine’s Techland.

![]()

Is iOS7 an earth-shattering development? I’m not sure it is. While I don’t hate the new iOS7 look, the Fisher-Pricey scheme of things stops me from liking it too much. There, I said it. Heck, my two-year old nephew has a toy phone that could pass off as the inspiration behind iOS7 – not kidding. The bright, fuschiously vibrant color scheme has sparked off many an internet meme, the most entertaining one being this one. That said, I’m not a designer, so I don’t want to sound like I’m biting off more than I can chew – but here’s a professional opinion specifically on the design elements of iOS7. Yes, design is a subjective thing and everyone is entitled to their own opinions; but if you go strictly by Steve Job’s own definition of it (see Para 2 above) – iOS7 leaves a lot to be desired.

Sure, it has cool interface improvements like a parallax view of the home screen (which lets a background image move around slightly while icons remain in place above it), swooshing transition animations, intuitive lock screens and transparent overlays. But unfortunately (for Apple) – there are other phones that have been doing that stuff (and more) for a while now. So does that mean that WWDCs are henceforth going to be only about tactics to level the playing field disrupted by some other player? Since when did Apple stop being the disrupter themselves?

Before I come across as a certified iRanter, let me state the key thing I want from the next iOS, in advance: All I want from the next iOS is more control. Maybe I’d like a search widget on my phone home screen. Maybe, a real-time RSS feed from Twitter. Maybe I’d like to change the static dock to feature the apps I actually access more often. Maybe I’d like the ability to choose my own default browser. Or maybe, I’d really like using a Swype keyboard on my phone (allowing me to swype through the keyboard as opposed to punching one key at a time). I’d like to at least have the option to make those tweaks, whether I exercise it or not. It is MY phone after all. I want it to “think different”, and be more of me, than of Apple. Too tall an order? Shouldn’t be so, right?

I’ve loved my iDevices for the sleek hardware and reliable software – I still sorta do. But from a competitive strategy perspective, both those competencies are now the stuff that is anyway expected of any smart device worth its salt. They’re necessary for succeeding in the market, but not sufficient anymore. Agreed, it was very much an Apple core competency to get the magical hardware + software combination right, but other players have started getting it right too.

Proponents of iOS7 and hardcore iFans have welcomed the end of skeuomorphism by saying it was redundant as it was the solution to a problem that Apple no longer has. While that may be true (and while I’m aware iOS7 is not just about skeuomorphism and also aims at providing a new user experience), I do tend to believe that the irony of iOS7 in turn is dual: A. It fails to address the problem(/s?) Apple actually has; and B. The bottle may have changed and become prettier (debatable adjective, perhaps!) – but the wine is sadly more or less the same.

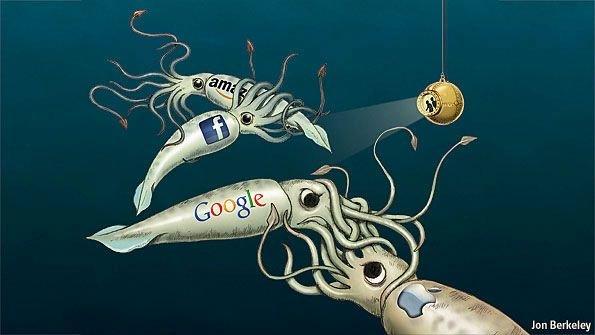

Clash of the titans

(Image source: iqballatif.newsvine.com)

The world of management consulting has its Big 4 – the accounting/professional services firms KPMG, Ernst & Young, Deloitte and PriceWaterhouse Coopers, the Goliaths that define the industry and make competitors in that space inconsequential and insignificant. Which is why it seems like quite a coincidence that the increasingly convergent world of technology and business too is dominated by four Goliaths: Amazon, Apple, Google and Facebook.

But is it really mere happenstance that the Big 4 of the business/technology world are just who they are? Probably not.

Over the years, the Big 4 have evolved from being simple product/service providers to comprehensive, repurposable platforms that shrewdly collate the required competencies of any online business:

- Data: Intelligence on Consumer Demographics, Actions/Behavior, preferences

- Devices: Desktop, Mobile, Tablet, and the Cloud

- Distribution: Collate, distribute and publish unique content

- Sociability:Sharability and conversation-worthiness

- Findability:Of accurate as well as geographically relevant information

The inherent similarity between the Big 4 is that they each are more an assortment of inter-related services (= Benefits and Values) than a singular product (= Feature). There is, of course, scope for improvement for each on these turfs and it’s not quite a level playing field across all product categories yet – a fact which they each are well aware of. Even so, as the Big 4 work on gaining competencies in new turfs and dialing up the aspects that they are not-so-competent in yet, the lines between categories, industries and software/hardware have increasingly started to blur. Here’s a strategic overview of how the Big 4 have been slowly yet steadily making forays into each other’s turfs.

AMAZON:

Last Quarterly Revenue: $13.8 bn | Last Quarterly Profit/Loss: -$274 mn | Market cap: $117.1 bn | Gross margin: 25.3% *

(Image source: http://www.teleread.com)

Amazon’s core competencies lie in E-Commerce, Distribution and Publishing. They have made a successful foray into the Device side of the platform via Kindle, and are rumored to be working on an Amazon phone that will be based on an Amazon-exclusive version of Android (“Amdroid”).The phone, like other Amazon extensions / diversifications will be aimed at ensuring you buy more from Amazon; and also provide Amazon more intelligence on your buying behavior and preferences – thereby supporting their core business.

What next? Amazon needs to become more responsive to competition. Until recently, Amazon played the role of Challenger well in the tablet market. But after Apple’s punch-packed response in the form of iPad Mini, the once-clearly defined boundaries between the target audiences of Apple’s iPad and Amazon’s Kindle have now blurred. Amazon will need to define the Kindle’s differential value (if any) better, and given that Amazon has been selling Kindle at a loss, either the price-point or the offering itself needs revision. There can be no doubt that Amazon has a bright future ahead, and the sheer length and breadth of its portfolio is astounding. Amazon is a shining beacon of service-orientation; where service-orientation is actually the common denominator across the architecture, culture and operations of the company. Another unique aspect about Amazon is its symbiotic relationship with a co-member of the Big 4 – Google. However, the extent of their dependence on Android (and thereby, Google), is potentially also a huge risk in the cut-throat context of the Big 4.

APPLE:

Last Quarterly Revenue: $36 bn | Last Quarterly Profit/Loss: $8.2 bn | Market cap: $489.3 bn | Gross margin: 40.2% *

2013 could prove to be a landmark year for Apple. As the most valuable company in the world, it has successfully made its presence felt across a good part of the tech ecosytem, ranging from hardware to software to distribution; Apple has yet to make a satisfactory mark for itself in the Search, Social and Data domains. To say their move to keep Google out of the geographical search domain out of the iOS sandbox has failed would be an understatement to an extent. Not only was Apple forced to bring Google maps back on iOS, they were also forced to come to terms with the reality that when it comes to anything Search (and Data collation related), Google is still very much the leader and Apple cannot claim to be a worthy challenger yet. Nonetheless, the reason 2013 could just be the year that features yet another genius innovation from Apple, is because Apple is working on converging Social , Data and Distribution together in a feature-loaded ‘iTV’, a move that tantamounts to bringing Apple, Facebook and Amazon together in your living room.

What next? If there’s a company that actually has the financial bandwidth to build a platform of interlinked products in the immediate future, it’s Apple. Apple gets platforms and has a great grip on consumer insights (well, at least so far). Apple is great at rocking the boat, and challenging the status quo, and improvising on the existing. However, Apple does not get the concept of ‘Openness’, be it Open access or Open source. The time to re-evaluate the boundaries of the ‘sandbox’ may be closer than Apple would like to admit. Also, times have changed, and the need of the hour is for Apple to play defense (ideally, in the market and not the courtroom!) all the while not losing steam on innovation.

FACEBOOK:

Last Quarterly Revenue: $1.26 bn | Last Quarterly Profit/Loss: -$59 mn | Market cap: $58.3 bn | Gross margin: 74.5% *

While Facebook is the leader in the sociability aspect of the game, findability is definitely a work-in-progress area for them. They’ve tried to upgrade their Search functionality in the summer of 2012, a move which has brought them a few steps closer to becoming a Social Search engine. Mark Zuckerberg offered a very matter-of-fact summary of the move: “Facebook is pretty uniquely positioned to answer the questions people have’ – and plans to build more powerful search facilities as Facebook evolves.” Key phrase to note obviously being, “uniquely positioned to answer the questions people have“. And in spite of the sheer goldmine of data that Facebook has at its disposal (Of course it does, who are we kidding!) – they have miles to go in actually leveraging that data effectively, beyond its already launched Facebook Ad Exchange and Facebook Ads targeted/retargeted advertising solutions.

What next? Facebook has access to the most-envied goldmine of consumer intelligence, and yet has always seemed to be indecisive and noncommittal about what it intends to do with it. Part of it is attributable to the fear of public backlash against using that data, but most of it has actually been because of the lack of clear vision on the the matter. They seem to be in constant experimental mode here, and that may prove to be detrimental to their cause.

GOOGLE:

Last Quarterly Revenue: $14.0 bn | Last Quarterly Profit/Loss: $2.2 bn | Market cap: $233.1 bn | Gross margin: 53.7% *

A key fact to keep in mind when we evaluate Google, is that as far as search goes – it is still a Google world. Per a December 2012 comScore report, Google owns about 67% market share, while the second-in-line Bing trails at a distant 16.2%. The

Android vs iOS

other trump card Google has in its repertoire is Android. The International Data Corporation (IDC) reported that 3 out of every 4 smartphones shipped out in the third quarter of 2012 were Android-based. Meanwhile, Google Plus, as we know is Google’s not-so-successful attempt at conquering the world of social networking. While the API-starved network may have well become Google’s very own ghost-town, there’s reason to believe that Google Plus could evolve into the product that is the face of the Google platform – given how Google has begun unleashing its Search horsepower and content ranking capabilities on Google Plus, along with the integration of other unique features like hangouts, circles and other weapons from Google’s holisitic arsenal.

What next? Google has its groundwork in place as far comprehensive platforms go. They have been shrewd enough to preempt the universal applicability of their main source of livelihood: Search (and Data-based intelligence). And they have been clever in initiating the open source/ Android movement years ago to restore balance in the i-Dominated smartphone world. They need to, however, ramp up their competencies in distribution/publishing and also social. Most importantly, they need to invest resources in developing well-rounded products that are actually good-to-go, as opposed to launching knee-jerk reactionary products (case in point: Google Plus) and then developing them on-the-go. Google needs to now prove that as far integration goes, they’ve still got it.

Now here’s a quick infographic to gauge how the respective platforms of the Big 4 stack up against each other.

The argument about who is destined to win this clash will probably continue for a while. But it is clear that the player that will emerge a true winner from this clash will not be the one that launches the most innovative product of the decade, but the one that manages to integrate all its products into a single, tightly knit ecosystem that creates perceptible value for the consumer. Each of the Big 4 likely stands an equal chance of being able to crack this code – or maybe not. In any case, there are exciting times ahead for sure – for technology, innovation and business in general. And whoever the winner proves to be, my hope is that in the end, it is we the consumers who gain the most from this epic clash of the titans.

* Key financials sourced from The Wall Street Journal

{kind=link}